Explore our Services >>>

INSIGHTS & RESOURCES

VIEW ALL INSIGHTS & RESOURCES

October 09, 2023

Beacon Weekly Investment Insights 10.9.23

Portfolio Manager, Charles Pawlik, CFA, CFP®, provides insights to guide you through changing market conditions. Please read the full text below or download the PDF version.

In what was an eventful week from a variety of perspectives, equity markets for the most part managed to end last week in positive territory with a sharp reversal on Friday in the wake of the release of the US employment report. The S&P 500 closed the week up 0.47%, with the Nasdaq up 1.60%. However, the Dow Jones Industrial Average finished the week in slightly negative territory, down -0.29%. Equity markets, amongst other things, continue to grapple with a significant move up in rates in the short-term as well as the notion of higher rates for longer. Oil prices, after rising for quite some time, dropped meaningfully last week in the midst of this dynamic and broader concerns over a slowdown, with WTI Crude oil down 8.8% for the week. Although concerns over higher rates and an economic slowdown have continued to mount more recently, the environment by and large remains one in which the broader economy has continued to prove more resilient than expected, and in which inflation, although having moderated, remains at roughly double the Fed’s target.

Underscoring the more resilient than expected economy, has been a continually tighter than expected labor market. Last week saw the release of the ADP employment report on Wednesday, and the more closely watched U.S. employment report was released on Friday. The ADP report showed a larger than expected increase in payrolls of 177,000, relative to the expectation of 160,000. Markets reacted to what was a significant upside surprise in the U.S. employment report released last Friday. The U.S. Economy created 336,000 jobs in September vs. expectations for 170,000 jobs. The U.S. unemployment rate remained unchanged at 3.8% vs. expectations for a tick down to 3.7%, with the labor force participation rate also remaining unchanged at 62.8%. The report showed strength across several sectors, including continued strength from leisure and hospitality with 96,000 jobs added. Importantly, average hourly earnings were up by 0.2%, which was less than the expected 0.3% increase. Equity markets initially turned down meaningfully after the report, as markets digested the significant upside surprise, likely initially reaffirming the idea of higher rates for longer. Yields were up across the curve, with the 10-yr. yield continuing its ascent and pushing through 4.80%. Fed funds futures initially priced in somewhat of a higher probability of a Fed rate hike by year end. However, equity markets subsequently recovered to close the day meaningfully positive, likely focusing on the continued resiliency of the economy, the lower than expected increase in average hourly earnings, and perhaps the idea that the Fed may not have to hike rates again as the significant tightening that has occurred in the bond market over a short period of time may be doing the work for them.

The JOLTS (job openings and labor turnover survey) report that came out last week had some conflicting information to the otherwise hot jobs market data, providing some signs of potential cooling in the labor market. The report detailed a higher than expected amount of job openings in August, coming in at 9.6 million, up from 8.9 million in the prior month and relative to expectations for 8.8 million job openings. In addition, the number of people quitting their jobs continues to moderate, and came in below 4 million for the third month in a row.

Markets also continue to grapple with uncertainty on the political front, as well as with the on-going strikes now occurring across several different sectors of the economy. With Kevin McCarthy having been ousted from the speakership, there is on-going uncertainty around a potential government shutdown. A new spending bill will need to be passed by mid-November to avert a shutdown. House majority leader Steve Scalise and Rep. Jim Jordan have thrown their hats in the ring to become the next Speaker of the House, setting up a possible vote for this week. The UAW continues its strike amidst negotiations for substantial pay hikes for its members, as well as other concessions. Some progress seems to have been made as Ford put forward a plan that further closes the pay gap in terms of what the UAW is seeking, however UAW Mack Trucks union members will now be joining Detroit autoworkers on strike. Last week also saw the initiation of a strike of 75,000 workers from Kaiser Permanente, which is the largest strike in history in the healthcare sector.

Conflict broke out in the Middle East over the weekend, as the Palestinian Islamist group Hamas launched an assault on Israel, sparking retaliatory air strikes on Gaza and a formal declaration of war from Israel. The attack comes in the midst of on-going peace talks between Saudi Arabia and Israel. Israel is said to be planning to call up 300,000 reserve soldiers as battles with Hamas enter their third day. Geopolitical events such as this tend to cause short-term volatility, broadly putting pressure on risk assets as the uncertainty over the duration and potential impacts of the conflict weighs on markets. While the underlying supply/demand dynamic for oil has not been immediately affected, conflicts in the Middle East tend to lead to an increase in oil prices in the short-term. There were reports that Saudi officials communicated to the White House that they may be willing to raise output next year as part of a proposed Israel deal. Along with impacts on the peace talks between Saudi Arabia and Israel and any potential increases in oil output as a result, questions as to whether or not Iran will be implicated in the conflict as well as potential impacts on transit through the Strait of Hormuz if wider conflict breaks out, will be focal points in terms of putting upward pressure on oil prices. After last week’s over 8% drop in WTI crude oil, prices jumped as much as 5% after the attack. As is also typically the case when conflict breaks out, major defense contractors traded up sharply. Assets that are perceived as safe havens and are generally expected to serve as a ballast when equity volatility breaks out such as gold and bonds, are both trading in firmly positive territory as of the time of this writing, underscoring the importance of diversification.

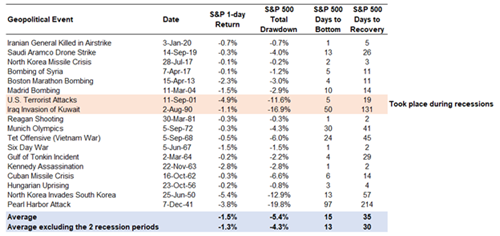

Geopolitical events such as this cannot be predicted and we do not suggest being reactionary, attempting to time markets, or chasing price spikes in assets that tend to benefit in the short-term amidst conflicts such as this. Although the uncertainly around the impacts of these types of events drives volatility in equity markets in the short-term, as detailed in the chart below, the impacts tend to be short-lived. As shown in the chart below, the average 1-day return for the S&P 500 in the wake of major geopolitical events was -1.5%, the average total drawdown was -5.4%, with the market taking 15 days to bottom and just 35 days to recover on average. Likewise, the S&P 500 dropped 6%-7% in the days and weeks subsequent to Russia invading Ukraine on February 24, 2022. However, a month later the S&P 500 had recovered and was trading at a higher level than prior to the invasion. These types of events as well as the backdrop of on-going uncertainty on many fronts, reaffirm why we continue to believe that the best way to navigate the markets for our clients is to remain invested in a diversified portfolio that has exposure to many different types of assets and opportunity sets as well as solid companies that can well navigate the environment, that is designed to meet client objectives and manage risk over the long-term, as well as consistently focus on maintaining sufficient liquidity in client portfolios so that we do not have the need to sell stocks at the wrong time.

As we look forward, earnings season will kick off this week with big banks such as JP Morgan and Citibank set to report on Friday. Overall, the earnings picture is expected to improve from the negative aggregate earnings for the S&P 500 in the first two quarters of the year. Although coming in better than expected, aggregate S&P 500 earnings were down by roughly -5.5% in the 2nd quarter. Earnings for the 3rd quarter for the S&P 500 are expected to be slightly positive, with expectations for roughly 8% earnings growth in the 4th quarter. Market participants will be paying very close attention to management commentary in terms of their outlook for earnings, cash flow, and margins in the coming quarters, with expectations that the economy will slow.

From an economic data standpoint, markets will be focused on both the PPI (produce price index) and CPI (consumer price index) reports, which are schedule to provide the next read on inflation on Wednesday and Thursday, respectively. Minutes from the Fed’s September FOMC meeting are also due out on Wednesday, with consumer sentiment data due out Friday.

Source: Bloomberg Intelligence

Source: Bloomberg Intelligence

|

Market Scorecard: |

10/6/2023 |

YTD Price Change |

|

Dow Jones Industrial Average |

33,407.58 |

0.79% |

|

S&P 500 Index |

4,308.50 |

12.22% |

|

NASDAQ Composite |

13,431.34 |

28.33% |

|

Russell 1000 Growth Index |

2,733.15 |

26.64% |

|

Russell 1000 Value Index |

1,473.88 |

-1.55% |

|

Russell 2000 Small Cap Index |

1,745.56 |

-0.89% |

|

MSCI EAFE Index |

1,993.63 |

2.56% |

|

US 10 Year Treasury Yield |

4.78% |

90 basis points |

|

WTI Crude Oil |

$82.79 |

3.15% |

|

Gold $/Oz. |

$1,830.20 |

0.22% |