Explore our Services >>>

INSIGHTS & RESOURCES

VIEW ALL INSIGHTS & RESOURCES

May 23, 2022

Beacon Weekly Investment Insight 5.23.22

Head of Chief Investment Officer, John Longo, PhD, CFA, provides insights to guide you through changing market conditions. Please read the full text below or download the PDF version.

The S&P 500 increased less than 1 point on Friday, but not before briefly dipping into bear market territory, which is commonly defined as a 20%+ drop from peak to trough. Will this be the shortest bear market in history? It’s hard to say with certainty, but the odds are against it. More on this in a moment. What we can say with greater clarity is that no one can consistently time the market, so sticking to a long-term financial plan is usually the best course of action. Successful market timing requires calling a market top and a market bottom, and for many clients, paying taxes on several years of capital gains.

Some market drawdown history. The average intra-year drop over the past 40 years has been about 14%, but the market wound up in positive territory about 75% of the time on a calendar year basis. There have been several periods in recent history (2010, 2011, and 2018) where the S&P 500 fell more than 15% intra-year, resulting in a severe correction, yet the bull market rolled on.

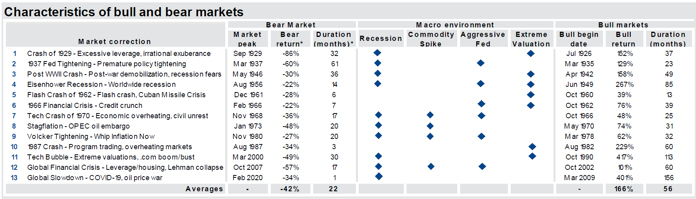

As shown in the table below, all bear markets are different. The COVID induced bear market of 2020 lasted a mere one month, before the market recovered, resulting in an amazing +16% return for the S&P 500 during that extraordinary year. Looking at periods since the 1950s, which we believe are the best comparables, the average duration of a bear market is 13.5 months, but 40% lasted less than 7 months. In our view, the period that most parallels the current one is the Volker Tightening – Whip Inflation Now period. The Federal Reserve at the time was trying to tame rampant inflation by raising interest rates. Sound familiar?

Source: JP Morgan

It took a while for Paul Volker’s Fed to get inflation under control, resulting in a double dip recession, one in 1980 and the other in 1982. Current projections for GDP Growth in 2022Q2 are around 1.5%-2.0%, despite the current inflation problem, so it is not clear that we are in another recession. If so, it would be short on the heels of the 2020 COVID induced recession, hence the 1980-1982 parallel.

Stocks have fallen for seven consecutive weeks, the first time it has achieved this dour milestone since 2001. For much of 2022, growth stocks have been pummeled. Last week, retailers took it on the chin, with Walmart, Target, and Ross Stores experiencing their biggest daily drops in years. For Target, their 27% plunge on Wednesday was the biggest since the Crash of 1987. In their respective earnings calls, executives from these firms made it clear that inflation is taking a toll on consumers’ budgets, especially for those on the lower end of the income spectrum. In general, consumers are spending less on many discretionary items and switching to cheaper generic brands when possible. As always, earnings reports are a mixed bag. As earnings season comes to a close, Palo Alto Networks, Foot Locker, and Synopsis each delivered stronger than expected earnings and outlooks.

If there is a small silver lining in the recent stock market volatility, it is that long-term interest rates have started to fall, providing a modest boost to diversified portfolios. For example, the 10 Year U.S. Treasury Note ended the week at 2.79%, down from its multi-year peak of 3.17% achieved less than two weeks ago. The drop in long-term rates should help the mortgage and housing markets, which have noticeably slowed in recent weeks.

As we head into the Memorial Day weekend, this week’s Economic Calendar will likely take a backseat to the financial media discussion about the possibility of a new bear market and its related investment implications. Nevertheless, the forward-looking S&P Purchasing Managers Indexes will be released on Tuesday. Durable and capital goods orders will be released on Wednesday, providing a clue on the status of long-term investments, which often decline in recessions. Weekly jobless claims feed into the monthly unemployment report and will be released on Thursday. The Personal Consumption Expenditures (PCE) gauge, an alternative measure of inflation, will be released on Friday. Given the intense focus on inflation by market participants, it will likely be the most important economic news release of the week. Also on Friday, the University of Michigan will release the finalized version of its Consumer Confidence Index. Spurred by high inflation and war in Eastern Europe, this sentiment index is expected to remain at recessionary levels. We wish you a wonderful Memorial Day Weekend and a brief respite from the cacophony of negative financial headlines.

|

Market Scorecard: |

5/20/2022 |

YTD Price Change |

|

Dow Jones Industrial Average |

31,261.90 |

(13.97)% |

|

S&P 500 Index |

3,901.36 |

(18.14)% |

|

NASDAQ Composite |

11,354.62 |

(27.42)% |

|

Russell 1000 Growth Index |

2,244.42 |

(27.01)% |

|

Russell 1000 Value Index |

1,492.34 |

(9.87)% |

|

Russell 2000 Small Cap Index |

1,773.27 |

(21.02)% |

|

MSCI EAFE Index |

1,969.24 |

(15.70)% |

|

US 10 Year Treasury Yield |

2.787% |

128 basis points |

|

WTI Crude Oil |

$112.70 |

49.37% |

|

Gold $/Oz. |

1,845.10 |

(0.80)% |